A severe storm just rolled through your neighborhood, and now you’re staring at missing shingles and water stains on your ceiling. The question racing through your mind: does homeowners insurance cover roof replacement, or are you facing a major out-of-pocket expense? It’s a concern that affects millions of property owners each year, and the answer isn’t always straightforward.

The truth is, coverage depends on several key factors, the cause of the damage, your policy type, and even the age of your roof. Insurance companies distinguish between damage caused by sudden events (like hail or fallen trees) and gradual wear from neglect or aging. Understanding these distinctions before you file a claim can save you time, stress, and potentially thousands of dollars.

At Sunflowers Energy LLC, we handle roof repairs and replacements for homeowners navigating this exact situation. Our team provides free on-site inspections and helps clients through the insurance claim process, ensuring you know exactly what’s covered before any work begins. This guide breaks down what your policy likely covers, what it doesn’t, and how to maximize your chances of a successful claim.

Why roof replacement coverage feels confusing

Insurance policies rarely give you a simple yes or no answer when it comes to roof claims. Most homeowners discover this the hard way after filing a claim, only to face unexpected claim denials or reduced payouts. The confusion stems from how insurers classify roof damage, which hinges on factors like timing, cause, and your roof’s condition before the incident. Even identical damage on neighboring homes can result in wildly different claim outcomes.

"The same storm damage that gets approved for your neighbor might be denied for you based on your roof’s age or maintenance history."

The gray area between damage and wear

Adjusters walk a fine line between sudden damage (covered) and gradual deterioration (not covered). You might see missing shingles after a windstorm, but if the adjuster determines your roof was already in poor condition, they’ll likely classify it as pre-existing wear. Insurance companies use depreciation schedules based on your roof’s age, which means a 20-year-old asphalt shingle roof gets far less coverage than a 5-year-old one, even if the same storm hits both homes. This depreciation factor alone can reduce your payout by thousands of dollars.

Policy language creates uncertainty

Your policy document likely contains phrases like "sudden and accidental," "acts of God," or "perils covered." These terms leave room for interpretation, and what you think qualifies as covered damage may differ significantly from your insurer’s assessment. The question "does homeowners insurance cover roof replacement" doesn’t have a universal answer because every policy has different exclusions, deductibles, and coverage limits. Some policies provide actual cash value (your depreciated roof’s worth), while others offer replacement cost coverage (full replacement regardless of age). Understanding which type you have makes all the difference when filing a claim.

What homeowners insurance covers for roof replacement

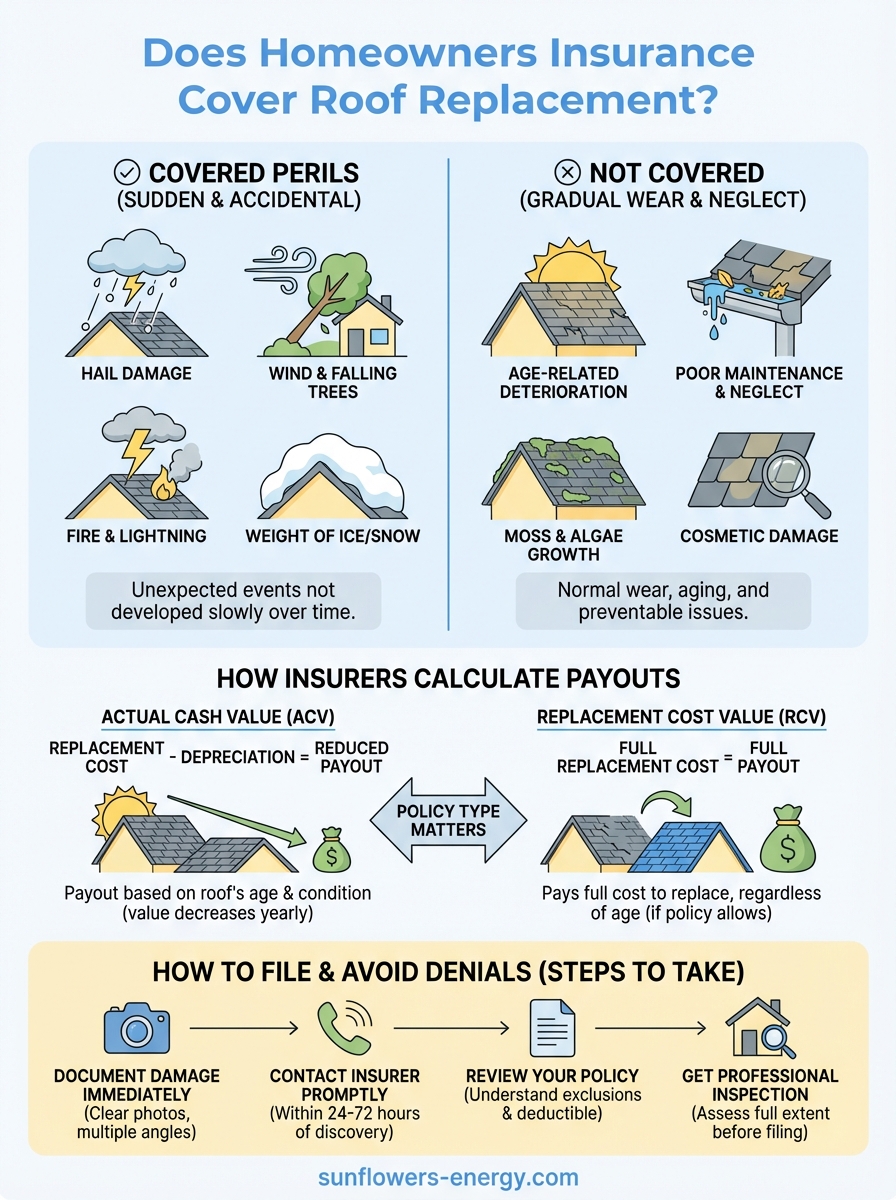

Your homeowners insurance typically covers roof replacement when specific covered perils cause sudden, accidental damage. Most standard policies protect against events like hail storms, wind damage, falling trees, fire, lightning strikes, and vandalism. The key distinction: the damage must happen unexpectedly, not develop slowly over time. When a tree branch crashes through your roof during a storm, that’s clearly covered. When your shingles gradually deteriorate from sun exposure over 15 years, that’s not.

"Insurance covers sudden events that cause damage, not the natural aging process of your roof."

Covered perils that trigger replacement

Wind and hail damage represent the most common covered claims for roof replacement. Policies typically specify minimum wind speeds (often 50-70 mph) that trigger coverage, and adjusters look for telltale signs like missing shingles, cracked tiles, or puncture damage from hail. Fire damage from lightning strikes, falling aircraft debris, or even riots also fall under standard coverage.

Weight of ice or snow can also qualify for coverage if it causes sudden structural collapse. The question of does homeowners insurance cover roof replacement comes down to whether your damage fits these sudden event criteria, not whether your roof simply needs replacement due to age.

What homeowners insurance usually will not cover

Insurance policies explicitly exclude damage that stems from normal wear and tear, neglect, or poor maintenance. If your roof reaches the end of its expected lifespan, you’ll pay for replacement yourself regardless of how diligent you’ve been about upkeep. Insurers consider aging a predictable expense, not an insurable risk. The question of does homeowners insurance cover roof replacement becomes irrelevant when deterioration happens gradually over years rather than hours.

Age-related deterioration and maintenance issues

Your policy won’t cover roofs that fail due to sun exposure, normal weathering, or lack of routine maintenance. Adjusters often deny claims when they find evidence of missing shingles you never repaired, clogged gutters that caused water damage, or moss buildup you ignored for years. Even if a recent storm causes the final failure, insurers trace the root cause back to deferred maintenance.

"Neglecting minor repairs today often leads to denied claims tomorrow."

Cosmetic damage and aesthetic concerns

Discoloration, fading, or minor cosmetic flaws don’t qualify for coverage even when storms cause them. Insurance protects your home’s structural integrity, not its curb appeal. You might notice algae stains or color mismatches after replacing storm-damaged sections, but insurers won’t pay to re-roof your entire home just to make the colors match. They’ll only replace the damaged portion, leaving you with potential aesthetic inconsistencies.

How insurers calculate roof claim payouts

Insurance companies use two primary methods to determine what they’ll pay when answering does homeowners insurance cover roof replacement: actual cash value (ACV) or replacement cost value (RCV). Your policy type drastically affects your final payout. ACV policies subtract depreciation from your roof’s replacement cost based on age and condition, while RCV policies pay the full replacement cost without deducting for depreciation. A 15-year-old roof might cost $15,000 to replace, but an ACV policy could pay only $7,500 after depreciation.

Depreciation schedules reduce your payout

Insurers apply standard depreciation rates based on your roof’s material and age. Asphalt shingles typically depreciate 5-10% per year, meaning a roof at 50% of its expected lifespan receives roughly 50% of replacement cost under ACV policies. Your adjuster calculates this by determining the roof’s original value, then subtracting depreciation for each year since installation.

"A 10-year-old asphalt shingle roof on a 20-year lifespan may only receive half the replacement cost under ACV coverage."

Your deductible and coverage limits apply

Your policy’s deductible amount gets subtracted from any payout, and coverage limits cap the maximum amount insurers pay. If your roof replacement costs $20,000 but your dwelling coverage limit is $18,000, you’ll face a shortfall even with full coverage approval.

How to file a roof claim and avoid denials

Filing a successful roof claim requires immediate action and thorough documentation. The moment you notice damage, you need to start building your case before weather conditions worsen or evidence disappears. Understanding the right steps helps you avoid the common pitfalls that lead to claim denials and ensures you get the maximum payout your policy allows.

Document damage immediately

Take clear, dated photographs from multiple angles showing the extent of damage to your roof, interior water stains, and any debris that caused the harm. Your photo evidence should capture both wide shots of the entire roof and close-ups of specific damage points like cracked shingles, dents, or punctures. Preserve any fallen branches, hailstones, or damaged materials as physical evidence your adjuster can examine during the inspection.

"Comprehensive documentation before repairs begin is your strongest defense against claim disputes."

Contact your insurer within required timeframes

Most policies require you to report damage within 24 to 72 hours of discovering it. Missing this deadline can result in automatic denial, regardless of how legitimate your claim is. When you call, request a written copy of your policy’s specific requirements and ask whether emergency repairs (like tarping) are covered before the adjuster arrives. Questions about does homeowners insurance cover roof replacement get answered faster when you provide detailed damage reports upfront rather than vague descriptions.

Next steps

Understanding whether does homeowners insurance cover roof replacement in your specific situation requires you to review your policy details and assess your roof’s current condition. Your coverage depends on the cause of damage, your roof’s age, and whether you maintain proper documentation. Taking action now puts you in a stronger position when you eventually need to file a claim, whether that’s after the next storm or years down the road.

Start by requesting a copy of your policy and identifying whether you have actual cash value or replacement cost coverage. Schedule regular roof inspections to document your maintenance efforts and catch minor issues before they become major problems that insurers won’t cover. When storm damage occurs, you need professionals who understand both roofing and the insurance claim process.

Sunflowers Energy LLC provides free on-site inspections and helps homeowners navigate the insurance claim process from start to finish. Our team documents damage properly, works directly with adjusters, and ensures you receive the full coverage your policy provides.

5 Responses