A bad storm rolls through, you spot damaged shingles, and now you’re staring down the State Farm roof claim process wondering where to even start. You’re not alone, roof damage claims are among the most common homeowner insurance filings, and getting the steps right from the beginning can make the difference between a smooth payout and a drawn-out dispute.

At Sunflowers Energy LLC, we work with homeowners through every phase of roof repair and replacement, including helping them navigate insurance claims after storm damage. We’ve seen firsthand how a clear understanding of the process, from that first phone call to final payment, saves time, stress, and money.

This guide breaks down exactly how to file a roof claim with State Farm, what to expect during the inspection, how payments work, and what to do if your claim gets denied. Every step is covered so you can move forward with confidence and get your roof back in shape as quickly as possible.

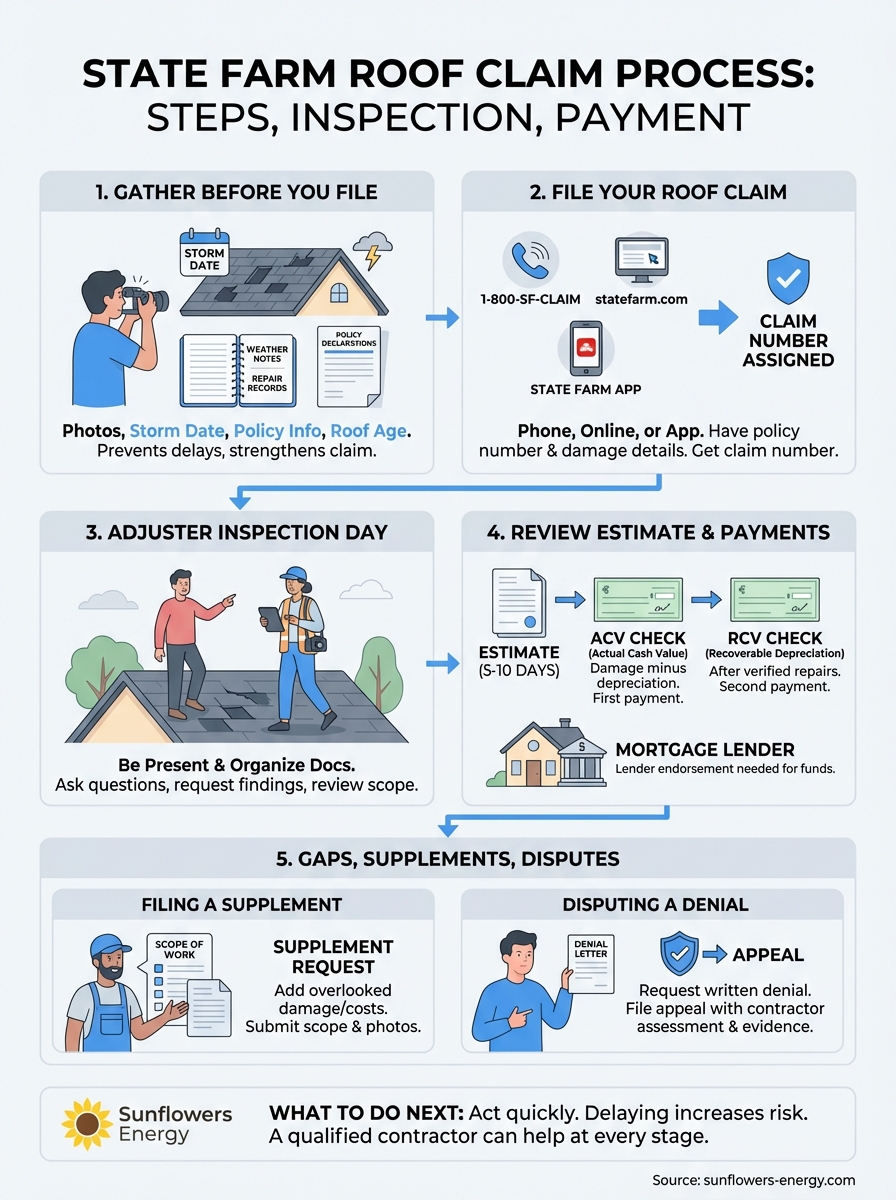

What to gather before you file

Before you contact State Farm, spending 20 to 30 minutes pulling together the right materials can prevent delays and strengthen your claim. Insurance adjusters work from evidence, and the more organized you are upfront, the less back-and-forth you will deal with later.

Having your documentation ready before you file sets a clear paper trail that protects you throughout the entire state farm roof claim process.

Your damage documentation

Start outside and photograph every visible sign of roof damage from multiple angles, including close-ups of missing shingles, dents on metal flashing, cracked tiles, and any water stains on interior ceilings or walls. Use your phone’s timestamp feature so every photo carries a date. If a storm caused the damage, note the exact date it occurred and check local weather reports to confirm the event.

Here is a quick checklist of what to capture:

- Photos of damaged shingles, flashing, gutters, and siding

- Interior water stains or ceiling damage linked to the roof

- Date and description of the weather event

- Any previous repair records or receipts for the roof

Your policy details

Pull out your homeowner’s insurance policy documents and locate your declarations page, which lists your deductible, coverage limits, and any exclusions. Knowing these numbers before you call means you will not be caught off guard during the conversation. Write down your policy number and keep it accessible because State Farm will ask for it immediately when you file.

Your roof’s age and material type are also worth noting if you have that information available. State Farm sometimes factors depreciation into claim payments based on how old the roof is, so having that detail ready gives you a clearer picture of what to expect from the payout.

Step 1. File your roof claim with State Farm

Once you have your documentation ready, filing your claim is straightforward and takes about 15 minutes if you have everything at hand. State Farm gives you multiple ways to file, so pick whichever option fits your schedule.

Starting the state farm roof claim process quickly after damage occurs matters because most policies require you to report damage within a reasonable timeframe.

Your filing options

You can reach State Farm through three main channels, each leading to the same outcome. Choose based on how much real-time guidance you want during the process.

- Phone: Call 1-800-SF-CLAIM (1-800-732-5246), available 24/7

- Online: Log into your account at statefarm.com and file through the claims portal

- Mobile app: Open the State Farm app, tap "File a Claim," and follow the step-by-step prompts

When you file, have your policy number, the damage date, and a brief description of what happened ready. A claims representative will assign you a claim number on the spot. Write it down immediately and save it in your phone because you will reference it to track every status update and communicate with your adjuster through the entire repair process.

Step 2. Get ready for the adjuster inspection

After you file, State Farm will schedule an adjuster to visit your property, typically within 3 to 10 business days. This step matters because the adjuster’s findings directly determine your payout amount in the state farm roof claim process, so preparation is worth the effort.

Being present and organized during the inspection gives you the best chance of a fair and complete assessment.

What to have ready on inspection day

Pull together your documentation before the adjuster arrives. Print your timestamped photos and organize them by damage type, then have your weather event notes and any prior repair receipts ready to hand over.

Here is a quick checklist:

- Timestamped photos of all damage areas

- Written record of the storm date and description

- Prior roof repair receipts or contractor reports

- Your policy declarations page

Be present and ask questions

Do not leave the adjuster alone during the inspection. Walk the roof with them, point out every damaged area, and ask them to explain what they are noting. Request a written copy of their findings before they leave so you have a record to compare against the estimate that follows.

Questions to ask on the spot:

- What specific damage are you recording?

- Are you documenting all areas I showed you?

- When will I receive the written estimate?

- What happens next?

Step 3. Review the estimate and payment timeline

After the inspection, State Farm will send you a written estimate outlining covered damage and repair costs, typically within 5 to 10 business days. Read every line carefully before accepting anything.

Pay close attention to whether your estimate lists Actual Cash Value or Replacement Cost Value, since that distinction directly shapes how much money you receive in the state farm roof claim process.

Understanding your payment breakdown

State Farm typically issues your first check for the Actual Cash Value (ACV), which equals the full replacement cost minus depreciation. Once your repairs are complete and you submit proof, they release the recoverable depreciation as a second payment. Here is how that timeline typically looks:

| Payment Stage | What It Covers | Typical Timing |

|---|---|---|

| First check (ACV) | Damage minus depreciation | Within 5-10 days of estimate |

| Second check (RCV) | Recoverable depreciation | After repairs are verified |

Working with your mortgage lender

If your home has a mortgage, your lender’s name appears on the claim check, which means you need their endorsement before you can use the funds. Contact your lender’s loss draft department right away to avoid delays. Most lenders require:

- A signed repair contract from your contractor

- The State Farm estimate

- Proof of completed repairs before releasing full funds

Step 4. Fix gaps, supplements, and disputes

The estimate you receive does not always cover every repair your roof needs. Adjusters sometimes miss damage, undervalue materials, or apply excessive depreciation. If your contractor finds additional damage during repairs, or if State Farm denies your claim outright, you have clear options to push back through the state farm roof claim process.

Staying organized and acting quickly gives you the strongest position when challenging an estimate or denial.

Filing a supplement

A supplement is a formal request to add overlooked damage or costs to your existing claim. Your contractor should provide a written scope of work that lists every item the original estimate excluded. Submit this document directly to your adjuster along with supporting photos and any contractor notes explaining why the additional work is necessary.

Disputing a denial

If State Farm denies your claim, request the denial in writing and review the specific reason they cite. Common grounds include wear and tear or a lapsed policy. You can file a formal appeal through State Farm’s claims department by submitting a written dispute letter, your contractor’s assessment, and weather event documentation.

- Written denial letter from State Farm

- Contractor’s written damage assessment

- Timestamped photos tied to the weather event

- Local weather records confirming the storm date

What to do next

You now have a clear map of the state farm roof claim process from documentation through dispute, and the most important thing you can do right now is act quickly. Delaying your filing or skipping the prep steps increases the chance of a reduced payout or a denied claim. Pull your photos together today, locate your policy number, and get your claim started through State Farm’s app, website, or phone line.

Working with an experienced roofing contractor makes every stage of this process easier. A qualified contractor can document damage accurately, write a detailed scope of work, and file supplements on your behalf if the initial estimate falls short. You do not have to navigate the inspection, estimate review, or dispute stages alone.

If your roof took storm damage and you need a professional assessment, contact Sunflowers Energy LLC for a free on-site inspection and estimate so you can move forward with confidence.

3 Responses