Going solar is a big financial decision, and how you finance it matters just as much as the panels on your roof. Mosaic solar loans are one of the most common financing options you’ll encounter when shopping for a residential solar installation, and for good reason. Mosaic has funded billions in clean energy projects across the U.S., partnering with thousands of solar installers to offer homeowners accessible loan products with various term lengths and rate structures.

But accessible doesn’t always mean straightforward. Mosaic’s loan agreements include details around dealer fees, interest rates, and UCC liens that can catch homeowners off guard if they don’t read the fine print. Online reviews are mixed, and comparing Mosaic to other solar lenders takes some digging. Whether you’re evaluating a quote that includes Mosaic financing or you’re an existing borrower managing your account, having clear information is essential before you commit.

At Sunflowers Energy LLC, we help homeowners navigate both the installation and the financing side of going solar. We believe an informed customer makes the best decisions, which is why we put this guide together. Below, we break down Mosaic’s rates, loan terms, lien structures, and real customer reviews, then show you how their offering stacks up against alternatives. By the end, you’ll have everything you need to decide whether a Mosaic solar loan is the right fit for your project.

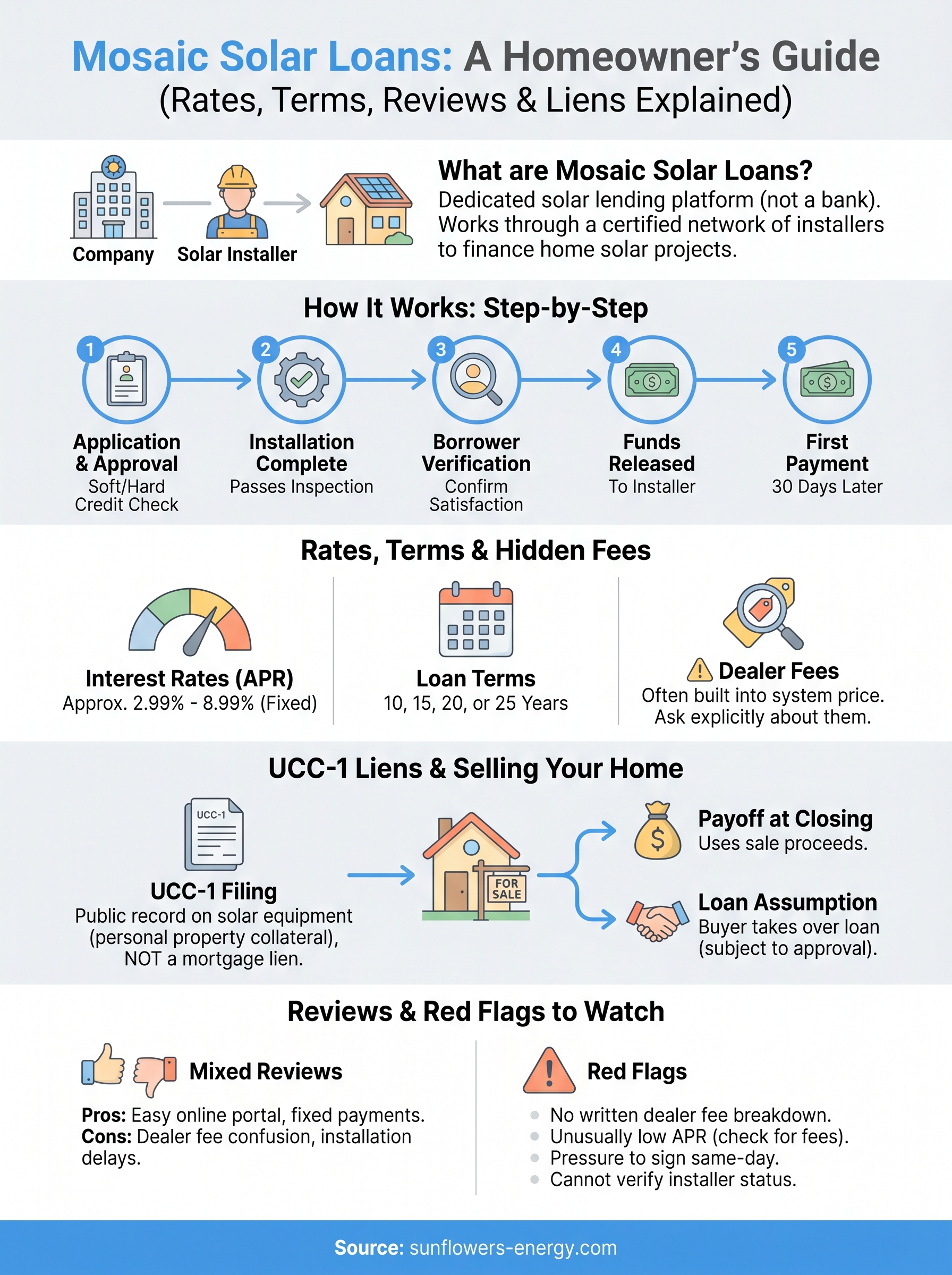

What Mosaic solar loans are and who offers them

Solar Mosaic, Inc. is a consumer lending company based in Oakland, California, focused exclusively on financing clean energy home improvements. Unlike a traditional bank or credit union, Mosaic doesn’t market loans directly to homeowners shopping online. Instead, they operate through a certified network of solar installers who present Mosaic financing as an option during the sales process. If you’ve received a solar quote that includes a monthly payment option, there’s a reasonable chance the installer presenting it works with Mosaic.

The company behind the loan

Mosaic was founded in 2012 and has since grown into one of the largest dedicated solar lending platforms in the United States. The company is not a traditional bank. It raises capital from institutional investors and deploys it as homeowner loans, which are then serviced under the Mosaic brand. If you take out a Mosaic loan, you’ll make your monthly payments directly through their online borrower portal rather than through your installer or a local bank branch.

Mosaic has funded over $10 billion in solar and home improvement loans since its founding, making it one of the most established dedicated solar lenders in the country.

Knowing who you’re actually borrowing from matters because your loan agreement, repayment schedule, and dispute resolution process are all governed by Mosaic’s policies, not your installer’s. Your installer handles the panels and the physical work on your roof. Mosaic holds the financial contract, which means billing questions, payoff requests, and account changes all go through them directly.

How Mosaic partners with solar installers

Mosaic recruits and certifies solar installation contractors across the country to offer their loan products to homeowners at the point of sale. Installers agree to Mosaic’s terms and complete a vetting process before they can present these financing options to prospective customers. This structure closely resembles how auto dealerships work with lenders to offer on-lot financing, where the buyer, dealer, and lender are three separate parties with different roles and responsibilities.

For you as a homeowner, this partnership means you can often secure financing and sign loan documents the same day you receive your solar proposal, without separately applying through a bank or credit union. Mosaic solar loans are available across most U.S. states, though availability depends on which certified installers operate in your area. Before signing anything, confirm that your installer is an active, verified Mosaic partner and request the full loan disclosure document so you understand every term before you commit.

How Mosaic solar loans work step by step

The loan process for mosaic solar loans follows a predictable sequence from the moment you receive a solar quote to the day your system powers on. Understanding each step helps you spot delays, ask better questions, and avoid surprises at signing.

From application to approval

Your installer submits a loan application on your behalf through Mosaic’s partner portal once you agree to move forward with a quote. Mosaic then runs a soft credit check to prequalify you, and if you proceed, a hard credit inquiry follows when you formally accept the loan terms. Approval decisions typically come back within minutes. Once approved, Mosaic sends you a loan agreement and disclosure documents via email, which you review and sign electronically before any installation work begins.

Read every page of your loan documents before signing, because the interest rate, loan term, and any dealer fee structures are locked in at this stage.

From installation to first payment

After you sign the loan documents, your installer schedules the physical work. Mosaic does not release funds to the installer until a few conditions are met: the installation is complete, the system has passed local inspection, and you have confirmed satisfaction through a borrower verification call or digital confirmation. This step protects you, because payment to your contractor only flows once the work is finished. Your first monthly payment typically becomes due 30 days after Mosaic releases funds to your installer, so your billing clock starts at project completion, not at signing.

Keep a record of your completion confirmation date, because that date determines when your repayment period officially begins and how your full payoff timeline calculates. If your installer drags out the installation, that delay directly shifts your payment start date, which is worth tracking from day one.

Rates, fees, terms, and eligibility to expect

Mosaic solar loans come in several configurations, and the specific terms you’re offered depend on your credit profile, loan amount, and the installer presenting the product. Mosaic is not a one-size-fits-all lender, which means two homeowners on the same street can receive very different rates and structures.

Interest rates and loan terms

Mosaic offers fixed interest rates that typically range from around 2.99% to 8.99% APR, though the low end of that range often comes attached to a dealer fee built into your installation price. Loan terms generally run 10, 15, 20, or 25 years, giving you flexibility to choose a monthly payment that fits your budget. Shorter terms mean higher monthly payments but lower total interest paid over the life of the loan.

If your installer quotes a very low APR, confirm whether a dealer fee is factored into your system price, because that fee can add thousands to your total cost even before interest applies.

Dealer fees and eligibility requirements

A dealer fee is a percentage that Mosaic charges your installer for offering their loan product. Installers commonly pass this cost to you by building it into the quoted system price rather than listing it as a separate line item. You won’t see it directly on your loan documents, but it inflates the amount you’re financing. Always ask your installer explicitly whether a dealer fee is included and how much it is.

To qualify for mosaic solar loans, you generally need a minimum credit score around 600, though better rates require scores in the 680 to 720+ range. Mosaic also requires proof of homeownership, as these loans are not available to renters. Income verification is typically part of the application review as well.

Liens, UCC filings, and selling a home with solar

When you take out mosaic solar loans, the financing agreement often involves a UCC-1 financing statement, which Mosaic files with your state government. This filing is not a lien on your home’s title in the traditional mortgage sense, but it does create a public record that Mosaic holds a security interest in the solar equipment installed on your property. Understanding what this means before you sign protects you from surprises later, especially if you plan to sell or refinance.

What a UCC-1 filing means for your property

Mosaic files a UCC-1 statement to protect its interest in the solar equipment as personal property collateral, separate from your real estate. This means the panels, inverter, and related hardware are technically Mosaic’s collateral until you pay off the loan. The filing shows up in a public records search, which title companies and mortgage lenders routinely perform during home sales and refinancing.

Buyers, title companies, and their lenders will flag an open UCC-1 filing during escrow, so you need a plan for resolving it before closing day.

How solar liens affect a home sale

Selling your home while carrying an outstanding Mosaic loan gives you a few options, and knowing them in advance saves time during escrow. You can pay off the loan balance in full at closing using proceeds from the sale, which triggers a UCC-1 termination filing from Mosaic. Alternatively, some buyers agree to assume the loan, taking over your monthly payments and inheriting the remaining term. Loan assumption requires Mosaic’s approval and a credit review of the incoming buyer. Request a loan payoff statement from Mosaic early in the listing process so your real estate agent and title company have accurate numbers from the start.

Reviews, red flags, and how to verify your lender

Customer opinions on mosaic solar loans are genuinely split, and the gap between positive and negative experiences often comes down to communication during the installation process and how clearly the loan terms were explained at signing. Homeowners who report positive experiences typically praise the straightforward online portal and predictable fixed payments. Those who report frustration most often cite confusion about dealer fees, delays in fund disbursement, or difficulty reaching customer service to resolve billing disputes.

What reviews actually say about Mosaic

Mosaic holds an average rating around 3.5 to 4 stars across major consumer review platforms, which is reasonable for a lending company but not exceptional. Positive reviews frequently mention that the application process is fast and that monthly payments are easy to manage once the loan is active. Negative reviews cluster around situations where the installer caused delays and the homeowner expected Mosaic to intervene, which Mosaic typically does not do because their role is financing, not project management.

Mosaic is your lender, not your contractor, so installation problems require you to resolve disputes directly with the installer, not through Mosaic’s support line.

Red flags to watch for before signing

Some warning signs are worth knowing before you commit to any solar loan, Mosaic or otherwise. Watch for these specific issues:

- No written breakdown of whether a dealer fee is included in your system price

- A quoted APR that seems unusually low without any explanation of how it’s structured

- Pressure to sign loan documents the same day you receive your quote

- Inability to contact Mosaic directly to verify your installer’s certified partner status

You can verify Mosaic’s licensing and complaint history through your state’s financial regulatory authority or the Consumer Financial Protection Bureau’s public database before signing anything.

What to do next

Mosaic solar loans give you a structured path to financing residential solar, but they work best when you go in with clear expectations about rates, dealer fees, and the UCC-1 filing that comes with your agreement. Before you accept any loan offer, request a full loan disclosure document and ask your installer directly about dealer fees built into your system price. If anything in the paperwork is unclear, contact Mosaic’s borrower support to get written clarification before you sign.

Choosing the right installer matters just as much as choosing the right loan. Working with a reputable local contractor who explains financing terms honestly and completes work on schedule protects you from the billing disputes and delays that drive the most common negative reviews. If you’re ready to explore solar for your home with a team that walks you through every step, get a free solar estimate from Sunflowers Energy LLC and we’ll help you understand your options from the start.